Geopolitics

Hormuz disruption exposes weaknesses in marine fuel supply, pricing and risk systems

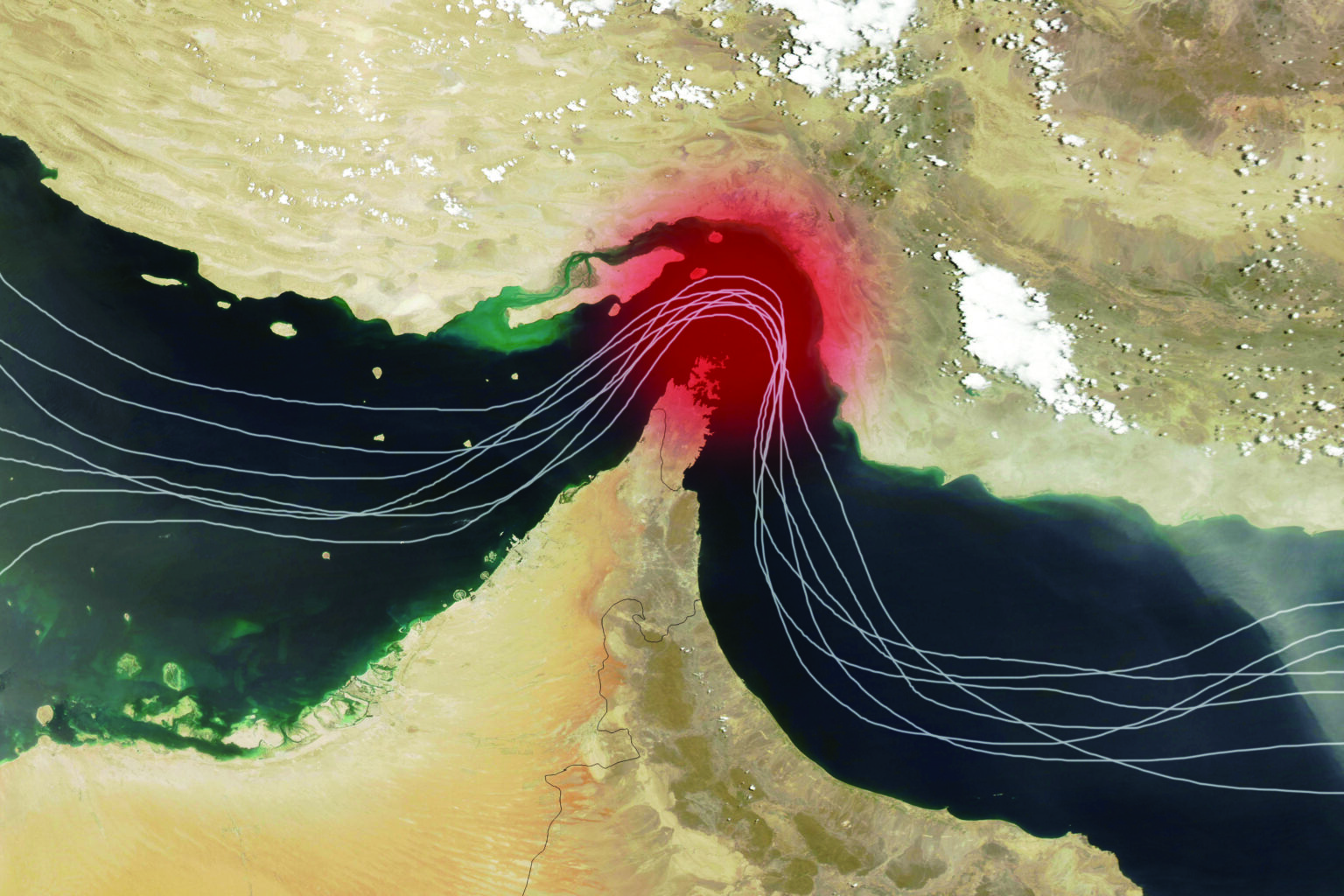

Hormuz closure tests bunker supply resilience

The closure of the Strait of Hormuz has turned the US-Iran war into a global energy, freight and bunkering shock. For marine fuel buyers and suppliers, the immediate concern has been price, but the wider issue is whether the industry’s supply chains, credit arrangements and risk-management systems are robust enough for a prolonged crisis.

A Global Chokepoint Under Pressure

The Strait of Hormuz has long been recognised as one of the world’s most important energy chokepoints. The International Energy Agency (IEA) says an average of 20 million barrels per day of crude oil and oil products moved through the Strait in 2025, representing around 25% of world seaborne oil trade. It also notes that 80% of those flows were destined for Asia, underlining the exposure of Asian economies and refining systems to any prolonged disruption.

The gas market is also exposed. The IEA says a closure would strand liquefied natural gas (LNG) exports from Qatar and the United Arab Emirates, which together account for almost 20% of global LNG exports. While Saudi Arabia and the UAE have some capacity to redirect crude away from Hormuz, other Gulf exporters remain heavily dependent on the route.

The economic effects are already visible. In its April 2026 Oil Market Report, the IEA said global oil demand was now expected to decline by 80 kb/d in 2026, compared with expected growth of 730 kb/d in the previous month’s report. It also estimated that demand fell by 800 kb/d year-on-year in March and by 2.3 mb/d in April, as higher prices and policy responses began to affect consumption.

The World Bank has described the conflict as a historic commodity-market shock. Its April 2026 Commodity Markets Outlook forecast a 24% rise in average energy prices this year and a 16% increase in overall commodity prices, with Brent expected to average $86/bbl in 2026. Its baseline assumes the most acute phase of disruption ends in May and that Hormuz traffic gradually returns close to pre-war levels by October, but it warned that risks remain tilted towards higher prices.

UN Trade and Development (UNCTAD) has taken a wider trade view, warning that higher energy, fertiliser and transport costs, including freight rates, bunker fuel prices and insurance premiums, may increase food costs and intensify cost-of-living pressures, particularly in vulnerable economies. ASEAN economic ministers have made a similar point, saying disruptions to Hormuz are increasing freight, insurance and logistics costs and could significantly slow regional growth.

From Oil Shock To Bunker Shock

For bunkering, the effect has been more complex than a simple pass-through from crude prices. Ship & Bunker reported that bunker prices rose sharply at all ports in March, with premiums to crude futures widening significantly after US and Israeli strikes on Iran and Iran’s closure of the Strait in response. By April, its G20-VLSFO Index averaged $890/mt, down 2.4% from March but still carrying a 16.3% premium to Brent, compared with 1.1% in the six months before the war.

Middle distillates have remained under particular pressure. Ship & Bunker said its G20-MGO Index gained 13.7% in April to average $1,606/mt, with the premium to Brent rising to 110%. The publication linked this to the importance of Middle Eastern refineries, and Asian refineries reliant on Middle Eastern crudes, in global distillate production.

There are signs that the first phase of panic buying and defensive pricing has eased. The Loadstar reported in mid-April that bunker shortage for containerships had not been as severe as initially feared, although prices remained high and local availability varied. It also quoted market participants in Singapore suggesting that ample stocks were available, even as some buyers questioned whether all price increases reflected genuine supply pressure.

That distinction matters. The crisis is not only a question of whether fuel exists, but where it is available, at what price, on what credit terms and with what operational certainty. Maersk said 20% of global fuel moves through Hormuz and introduced a temporary Emergency Bunker Surcharge from 25 March, saying the measure was needed to cover fuel availability, cost and mix outside its existing Fossil Fuel Fee. The surcharge applies globally, subject to regulatory approvals, and will be adjusted as fuel availability and cost change.

Hapag-Lloyd has also introduced an Emergency Fuel Surcharge for sailings from 23 March, with separate dry and reefer charges for long-haul and intra-regional trades. It has also applied war-risk charges for cargo linked to the Upper Gulf, Arabian Gulf and Persian Gulf. These measures show how bunker disruption is moving rapidly into freight contracts and customer-facing cost structures.

Alternative Ports And Changed Patterns

The closure has also changed the geography of bunkering demand. Dan-Bunkering’s late-March market report pointed to increased activity at ports such as Port Louis, Durban and Walvis Bay as vessels considered alternative routes and avoided higher-risk areas.

It noted much higher demand than before the crisis at Port Louis, selective fixing by suppliers in Durban and tightening availability in Walvis Bay.

Singapore appears to have been both exposed and resilient. Ship & Bunker said Singapore saw initial supply concerns in March, but these concerns later eased, partly because the port’s scale gives it the ability to pull supply from smaller regional ports and from further afield.

That does not mean it is insulated. Asian supply chains are more directly exposed to Middle Eastern crude than those in Rotterdam or Houston, which helps explain why the price effect has been uneven across major bunkering centres.

Risk, Quality And Counterparty Scrutiny

Industry sources suggest the next phase of the crisis may place more emphasis on risk control.

NorthStandard has warned that disrupted oil flows and tighter availability could push operators towards unfamiliar suppliers or sources. It said the less visible risk is fuel quality, including the potential use of unfamiliar cutter stocks and blending components.

That concern is familiar to the bunker sector. In a high-price market, buyers may be under pressure to accept unfamiliar counterparties, shorter notice stems or alternative specifications. That may increase the importance of supplier vetting, representative sampling, independent testing and clearer contractual language on quality and delay.

Safety is now part of the same calculation. IMO Secretary-General Arsenio Dominguez told member states and industry representatives on 24 April that there was “no safe transit anywhere” in the Strait of Hormuz.

The IMO said it had verified 29 attacks on vessels in the Persian Gulf and around the Strait since the start of the conflict, with at least 10 seafarers killed and around 20,000 seafarers remaining in the Gulf.

The International Chamber of Shipping has urged ships in the region to conduct thorough risk assessments, maintain vigilance and rely on verified information from trusted sources.

INTERTANKO has similarly advised members to follow Best Management Practices, monitor official guidance and, where possible, delay Hormuz transits until the situation is clearer.

Structural Shift For Marine Fuels

IBIA has framed the crisis as both immediate and structural. Its newly elected chair Adrian Tolson said that even if the situation were resolved quickly, the implications would not disappear.

He said concerns around energy security were likely to persist, with increased focus on diversification, including alternative fuels, and longer-term changes in how bunker supply and demand are structured.

Alexander Prokopakis, IBIA’s executive director, has also stressed the importance of safety-led messaging. He described political calls for tanker crews to transit the Strait as “highly problematic”, saying they clouded the industry’s message to prioritise caution at a time of extreme risk.

For the bunker industry, the lesson may be that resilience is no longer measured only by fuel availability at the quayside.

It also depends on diversified sourcing, transparent pricing, robust credit control, quality assurance and realistic contingency planning.

The Strait may eventually reopen, but many observers suggest the assumptions behind marine fuel procurement have already changed.

Image Credit: Adobe Stock

get

in touch

Constructive Media

Constructive Media

Hornbeam Suite

Mamhilad House

Mamhilad Park Estate

Pontypool

NP4 0HZ

Tel: 01495 239 962

Email: ibia@constructivemedia.co.uk

On behalf of:

IBIA London Office

Suite Lu.231

The Light Bulb

1 Filament Walk, Wandsworth

London, SW18 4GQ

United Kingdom

Tel: +44 (0) 20 3397 3850

Fax: +44 (0) 20 3397 3865

Email: ibia@ibia.net

Website: www.ibia.net

Emails

Publisher & Designer: Constructive Media

ibia@constructivemedia.co.uk

Editor: David Hughes

anderimar.news@googlemail.com

Project Manager: Alex Corboude

alex@worldbunkering.net